At this point in my life, I thought of wealth the way most of the world thinks of it: I exchange my time in the form of work for money, and I earn more money either by A) working more hours, or B) getting paid more per unit of time, or C) doing both. So goes the proverbial “rat race” to “maximize earning potential” because the more I EARN, the RICHER I am. Strive to get paid more. This is the path to financial riches, right?

Well…not quite…

Actually, your wealth is NOT determined by how much money you EARN. In fact, it might have little at all to do with the size of your paycheck.

Two Examples

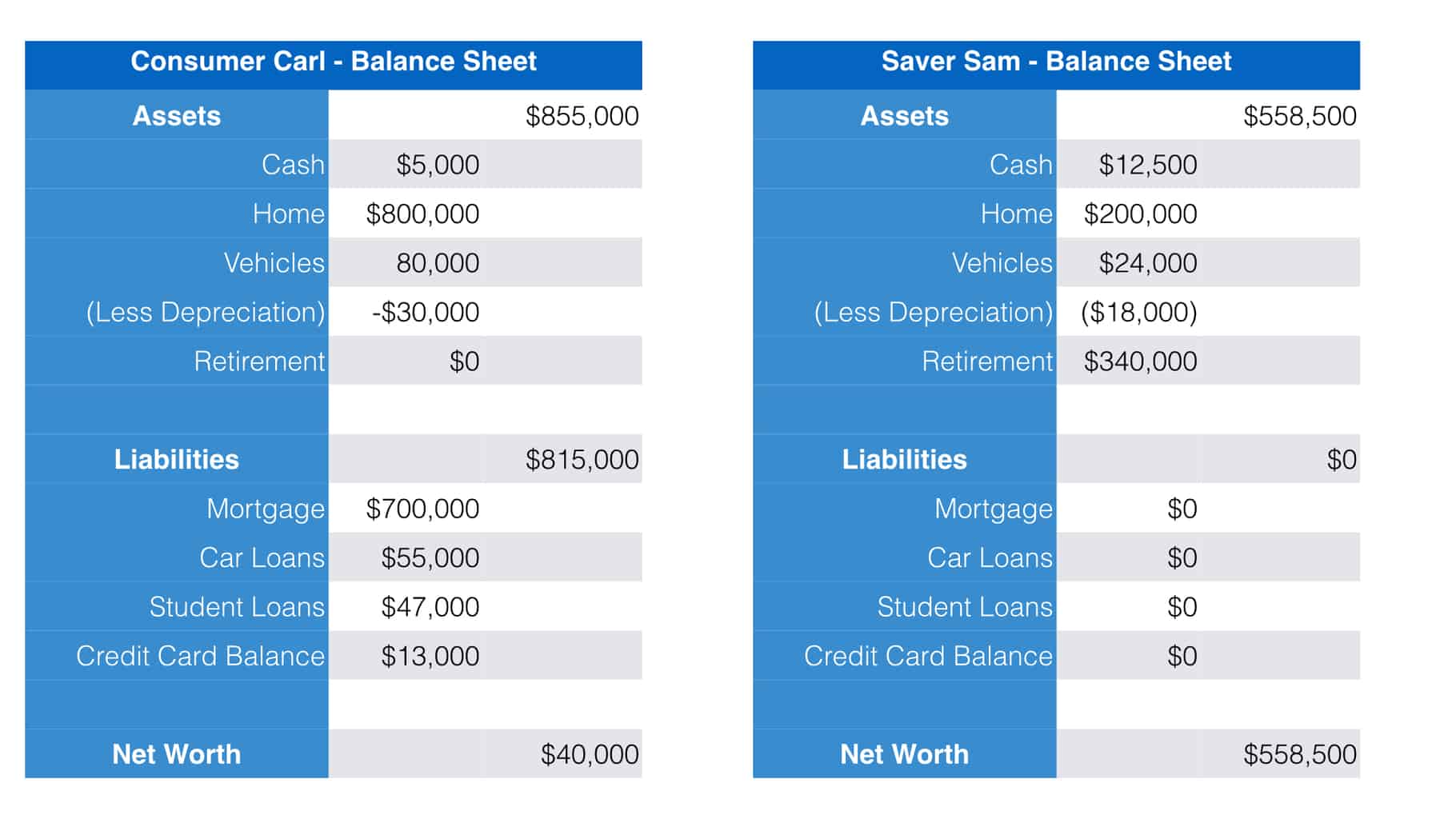

Consumer Carl is a medical professional in his fifties who makes $150,000 annually, well above the 2012 US national average of $44,000. He lives in a big house with an equally impressive mortgage and drives multiple fancy, financed cars. He and his wife eat out regularly and take international vacations annually. They have no retirement savings.

Saver Sam is a schoolteacher also in his fifties who makes $40,000 a year (below the 2012 US national average). He owns a modest, paid-for suburban home and he and his wife share an old, reliable Toyota Camry. They cook at home and rarely eat out, and their vacations are usually to visit family and friends. They’ve been diligent investors, preparing for retirement.

Which of these two individuals are wealthier?

Before you answer, let me give you a hint. This is a trick question.

It’s About the Net Worth

Most people looking in from the outside would pick Consumer Carl as the obvious winner of the two. And indeed he has higher likelihood of being so, but there simply isn’t enough information to determine that from this example.

The reason is because wealth is measured by NET WORTH, and not by the size of an income. The calculation of net worth is quite simple:

Net Worth = Assets – Liabilities

So to determine your own net worth, simply add up all the assets that you own (cash in the bank, stocks, retirement accounts, property, vehicles, businesses, etc.) and subtract from it all the liabilities (debts) that you carry. The result is the true measure of your wealth.

Notice that your monthly paycheck isn’t a part of this equation. Just think, even if you made $20,000 a month but spent every dime of it, you haven’t increased your net worth at all. Your income affects your net worth only by how much surplus you’re able to save.

So a “millionaire” is defined as someone who has over $1 million dollars of net worth and NOT as someone who earns more than $1 million in pay (even though those people would likely be millionaires too). Who cares what Warren Buffett’s salary is per year as CEO of Berkshire Hathaway? (It’s actually $100k per year, much less than our friend Consumer Carl.) It’s his NET WORTH that ranks him as one of the wealthiest men alive. (#3 on Forbe’s list at nearly $70 billion.)

Running the Balance Sheet

Two of the ways businesses communicate their financial health are through 1) the income statement also known as the profit/loss statement and 2) the balance sheet. (There’s also the cash flow statement, but that’s for another discussion.) The income statement is like a household budget, showing the revenue and expenses over a period of time; whereas the balance sheet shows the assets and liabilities of a company at a specific point in time. The bottom line of the income statement is the NET PROFIT, while the bottom line of the balance sheet is the NET WORTH.

We can apply these financial statements to the business known as OUR LIFE to help us get the pulse of our financial health too. My hunch is that most people are like me as a high school freshman, sweating over the income (“How much did I make this pay period and how much can I spend?”), while neglecting our personal balance sheet.

Let’s revisit Consumer Carl and Saver Sam again. We already know how much income they make, let’s take a look at their fictional balance sheets to see if we now have enough information determine which one is wealthier.

Changing Our Thinking

It was a light bulb moment when I realized that wealth isn’t measured by the size of our paycheck or even our net profit, but rather by our net worth. This changes everything. Rather than worrying (or complaining) about not getting paid enough, we should rather be focusing on increasing our rate of savings, increasing our assets, and decreasing our liabilities instead. Are we buying consumables that decrease in value, or are we buying assets that put our money to work for us, increasing in value? Are we spending everything we make each month or are we saving and investing? Do we have debt that cancels out our assets on our balance sheet? Or worse, do we OWE more than we OWN? Don’t get too enamored with your paycheck, show some love to your balance sheet too.

The Teddy Bear Lady

Gladys Holm worked as a secretary and never made more than $15,000 a year in her entire life. She was known as the “Teddy Bear Lady” because she would visit sick children at the Children’s Memorial Hospital in Chicago and give them teddy bears. When she died in 1996, she left more than $18 million to that hospital. The president of the hospital had to ask her attorney to repeat the figure because he was certain that he had misheard.

We would hardly consider someone making $15,000 (even back in her day) anywhere NEAR wealthy, but yet we all would agree that being worth $18 million is VERY wealthy! Gladys Holm demonstrates clearly the point that the size of one’s paycheck doesn’t necessarily determine one’s wealth.

So how did she do it? She learned to invest from her boss, and she simply persisted in consistently investing small amounts through her entire 41 years of employment–putting to work the secret ingredient of investing. In the end, her net worth was FAR higher than those making many times her salary.

True Wealth

The story of Gladys Holm is also a poignant reminder that whether we have $18 million or $18 to our name, sooner or later we’re going to die. To me, even more important than the dollar amount of her net worth, is what she did with her wealth. She knew that it wouldn’t do her any good in the grave so she blessed the world with it. Knowing the difference between net profit and net worth is good, but USING that profit and wealth to benefit the world is even better. That’s the reason why we’re saving the crumbs in the first place!

{kind=link}