Why Share So Much?

Many people have asked us why we’re so open in sharing our numbers like this, especially since we’re rather private people. Talking about money is taboo in most of US society, so it’s no wonder that people are surprised. We share our personal financial information for the simple reason that we feel it is the best way to actually help people. I can share theories and principles until I’m blue in the face, but there’s so much more power in saying, “This is what I ACTUALLY do.” Then the influence is further compounded when I can show through the objective measure of our real-life numbers our actual (hopefully successful!) results.

To say the same thing in an utterly non-politically correct way, we’re tired of hearing the wimpy, namby-pamby, complainy-pants excuses of people who lose control of their money (and consequently their lives). “It’s impossible to live on a budget!” “I’m too poor to give!” “I don’t have rich parents!” “My debt’s no big deal, everyone’s in debt!” “I have to spend money to have a life!” “It’s the government’s fault!” “It’s the economy’s fault!” “It’s everyone else’s fault!” “Poor me! Life’s so unfair!” “Blah, blah, waah, waah!” Rather than tear out our hair over the feigned financial victimhood we hear all the time, we thought we should just lead by example. People don’t need to be just like us (have mercy!), but by sharing our numbers, perhaps we can help bust this crazy myth that life is “so tough” for the middle class in a modern-day affluent country.

2014 in Review

A little background on our year:

- In 2014, both Deb and I continued working full-time in our respective nonprofit organizations as in 2013.

- 2014 was the first full year that we lived in our home which was purchased in August 2013.

- 2014 was also the first full year of collecting rent from the small guesthouse on our property.

- We did a fair amount of traveling this year. Our rough tally showed that we were on the road for about 3 months of the year, and the vast majority of that was business travel.

- Summaries of our situations in 2013 and 2012 can be found in the previous post: Our Finances Exposed

2014 |

2013 |

2012 |

|

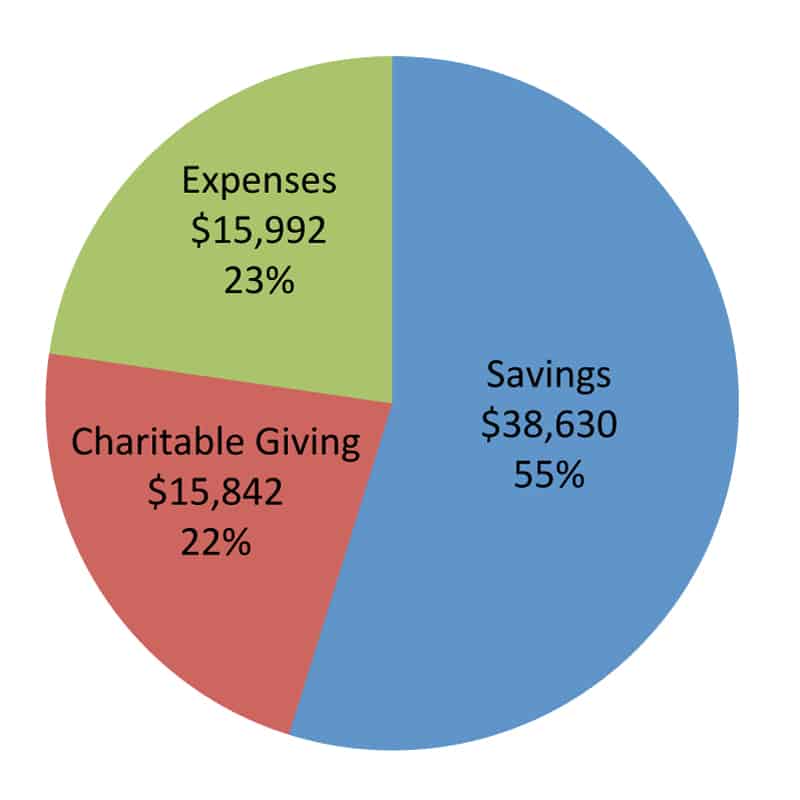

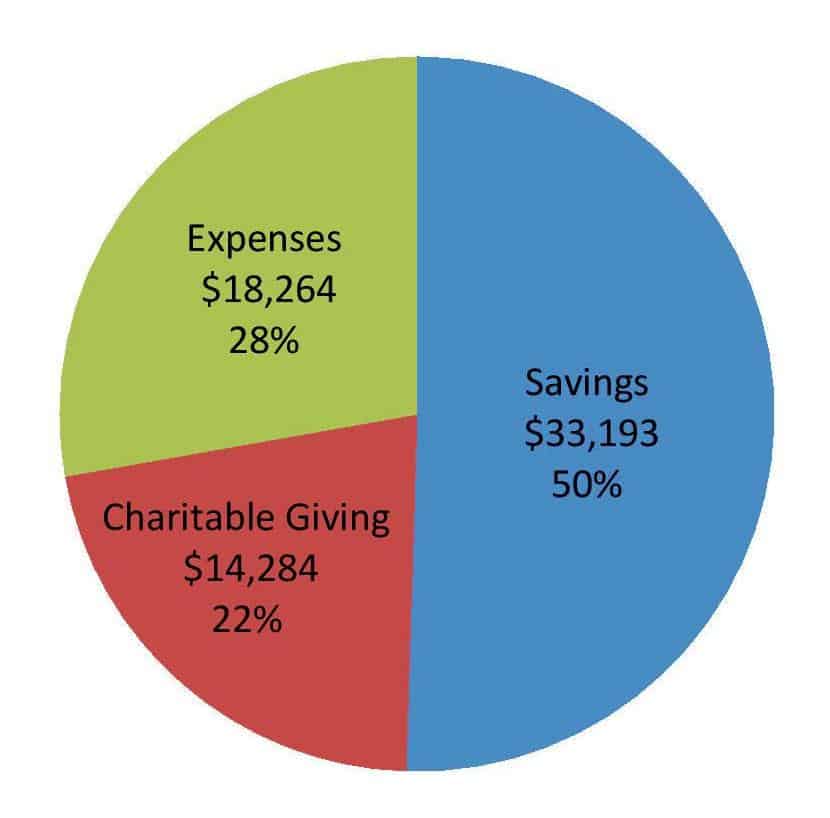

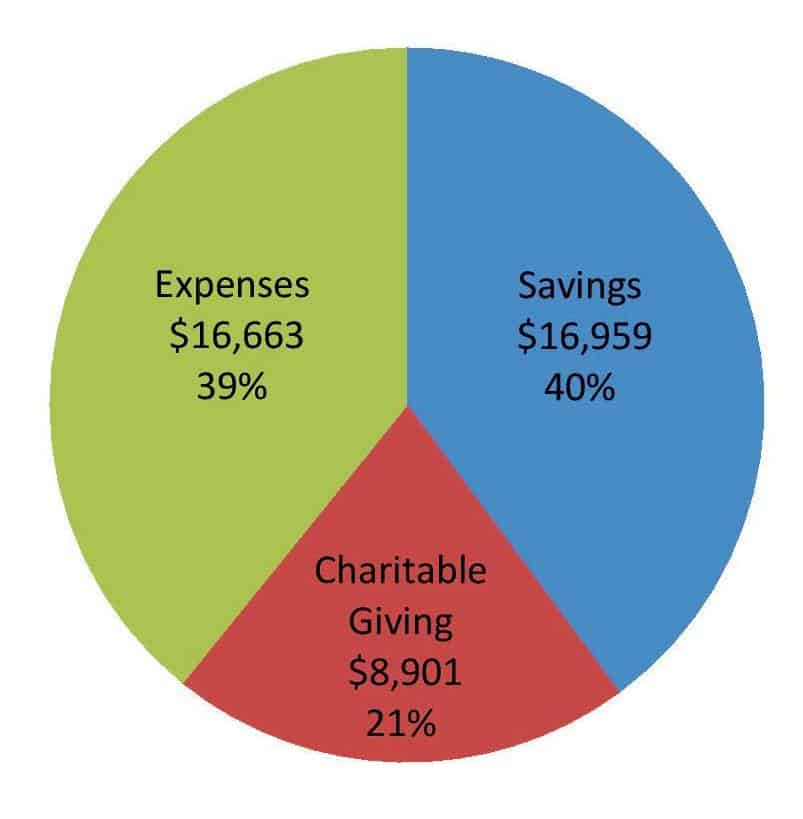

| Total Income: | $70,464 | $65,741 | $42,523 |

| Tithe/Charitable Gifts: | $15,842 | $14,284 | $8,901 |

| Living Expenses: | $15,992 | $18,264 | $16,663 |

| Net Income (Saved): | $38,630 | $33,193 | $16,959 |

| Percentage Saved: | 55% | 50% | 40% |

2014 |

2013 |

2012 |

|

|

|

- The income numbers represent after-tax income.

- Tithe/Charitable Gifts is the single largest expense in our budget so we break it out in order to give an accurate picture of what we spent to live. We practice the Biblical principle of tithing so we give 10% to our church, then after that we give another 10% to other ministries and charitable causes.

- Notice that even though our income increased from year to year, our living expenses did not. The percentage of income spent on living expenses decreased in 2013, and the absolute amount spent in 2014 was lower than BOTH 2013 and 2012!

- Yes, you read correctly that it cost less than $16,000 for the two of us to live in 2014. This includes all living expenses: Food, insurance, mortgage payments, running/maintaining the car, gifts, recreation, and everything except our business travel.

- Moreover, notice that the amount we spent to live was only $150 more than what we gave away for the entire year. In other words, what we gave away pretty much equaled how much it cost us to live. We were pleasantly surprised to see that.

- We saved 55% of our income, with all of that excess primarily going to pay off our house. Based on my calculations, it is slated to be paid off sometime this year, or about 2 years after we signed on the dotted line.

- Why spend so little and save so much? I’m so glad you asked! It has everything to do with the simple formula to get “rich“.

The Monthly Breakdown

| Categories | Annual Total | Monthly Average | Notes |

| Housing & Utilities |

$10,723.92 |

$893.66 |

Includes: Mortgage, home insurance, property tax, water, electricity, cellphone |

| Health Insurance |

$1,963.50 |

$163.63 |

We use a service called Christian Medi-Share which is a medical expense sharing program. |

| Automobile |

$1,610.02 |

$103.67 |

Includes: Gasoline, oil changes, vehicle maintenance, registration, insurance |

| Household/Supplies |

$738.00 |

$61.50 |

Includes: Household cleaning, tools, gardening, clothing, personal hygiene, and misc. |

| Groceries |

$599.76 |

$49.98 |

Includes our groceries, but not eating out. Dining out is classed under “Recreation”. |

| Recreation |

$356.99 |

$29.75 |

Includes: Eating out, gifts for people, and fun things. |

| Total: |

$15,992.19 |

$1,302.19 |

The Scoop

So how do we keep our living expenses so low? Well, we’ve been sharing some of our strategies steadily through the past year, so here’s a quick review along with some links to previous articles on the subjects:

- Mortgage – Our monthly mortgage payment is only $607.24. That’s possible because we had a massive down payment when we bought the house and we scored a nice 3.49% fixed rate. You can read about it in our post: 7 Lessons as One-Year Homeowners: And paying it off in less than 3 years. What’s amazing is that once our mortgage is paid off sometime this year, that will slice nearly $7300 off our living expenses per year. Meaning, we can potentially live for UNDER $10,000 a year!

- Water – Our monthly water bill has consistently been $10 every month since we moved in. This held true even when we had guests stay at our house. Check out our strategies on saving water in our post: How to Save Water.

- Electricity – We’ve written about how to save electricity in general, as well as specifically how to save on heating in winter (we have only electric heat). But our big electricity secret is that not only do we pay $0 for our electricity, but the power company actually PAYS US due to the solar panels we’ve installed. Curious? Check out my post on it here: How We Get Paid by Our Power Company with Solar Panels.

- Cellphone – At the end of 2014 my whole family switched over to a Group Save Plan with Cricket Wireless which now gives my iPhone unlimited calling, texting, and data for just $20 a month (this includes tax)! Read more about it here: Is Your Cellphone Plan Ripping You Off?

- Health Insurance – We use a Christian medical expense-sharing program called Medi-Share and it is vastly cheaper than equivalent coverage from Obamacare insurance options.

- Automobile – Some of the big reasons why our vehicle expenses are low (even though we drive a gas guzzling V6 Honda Accord) is because we keep our driving down to a minimum, we don’t finance depreciating assets like cars, and we can get by with much cheaper insurance since we drive an older car. Learn about the total cost of ownership for a vehicle, and you’ll better understand why you shouldn’t ever borrow money to buy a new one. If lower gas prices are here to stay, we look forward to this number going down in the future!

- Household/Supplies – We’ve gotten into the habit of reducing waste and reusing stuff around the house. The ideas are endless, but here’s just a sample of things Deb reuses in the kitchen: 7 “Not Their Original Purpose” Items in Our Kitchen. Oh, and we usually buy our clothes at thrift stores.

- Groceries – It may seem outrageous, but our food budget actually DECREASED from about $58/month in 2013 to $50/month in 2014. This can largely be attributed to the fact that we grew a bunch of food in our garden, plus we were on the road for nearly a quarter of the year. It wasn’t necessarily a goal of ours to cut our food budget anymore, but it just turned out that way. Check out Deb’s popular series on Eating for 90% Less than Your Neighbors for a full breakdown on our grocery strategy and check out these other helpful tips on shopping:

- 5 Steps to Find a Grocery Store that Saves You Money

- Why Aldi Should Be Your Best Friend (Check out the full series.)

- Why We Don’t Buy Costco Membership

- Recreation – It’s true, we don’t go out very much and when we do, it’s usually to do free stuff. What can I say? Entertainment and other such things are discretionary for us, and we’re just wired to enjoy saving money much more than spending it. Want proof? Check out how we celebrated our anniversary this past year: A Special Anniversary Weekend – Crumb Saver Style.

Conspicuous Absentees

There are two common categories of things that don’t exist in our spending and they are 1) Subscriptions (gym memberships, music subscriptions, TV subscriptions, magazine subscriptions, etc.) and 2) Consumer Debt (credit cards, car loans, student loans). These types of things are not only leeches to your finances, but they can be downright cancerous! Pay off your debt, cancel as many subscriptions as you possibly can, and you’ll be surprised how much you can free up your cash flow.

One Last Thing…

2014 was certainly a successful year for us in our financial goals. We spent less, gave more, saved more, and enjoyed it more than ever. And one big reason why is because of…YOU! You readers out there with your encouraging comments, earnest questions, and genuine interest have helped us stay the course. Not to mention, you’ve helped keep us accountable to actually practice what we preach! So THANK YOU for sticking with us and keeping us honest.

Looking forward to an exciting 2015!

{kind=link}